Advanced Tax Strategy for Self-Employed People: What Most People Never Get To

Educational overview only — not tax advice. Consult a qualified CPA for your specific situation.

If you’ve been tracking your business expenses, logging your mileage, and claiming your phone and internet as deductions — you’re doing the basics. And the basics matter.

But there’s a level of tax strategy beyond the basics that most self-employed people, side hustlers, and network marketers never reach. Not because it’s inaccessible. Because nobody walked them through it.

This post covers three advanced areas: entity structure, self-employed retirement accounts, and the home office deduction done properly. At the end, I’ll give you the specific questions to bring to your next CPA meeting.

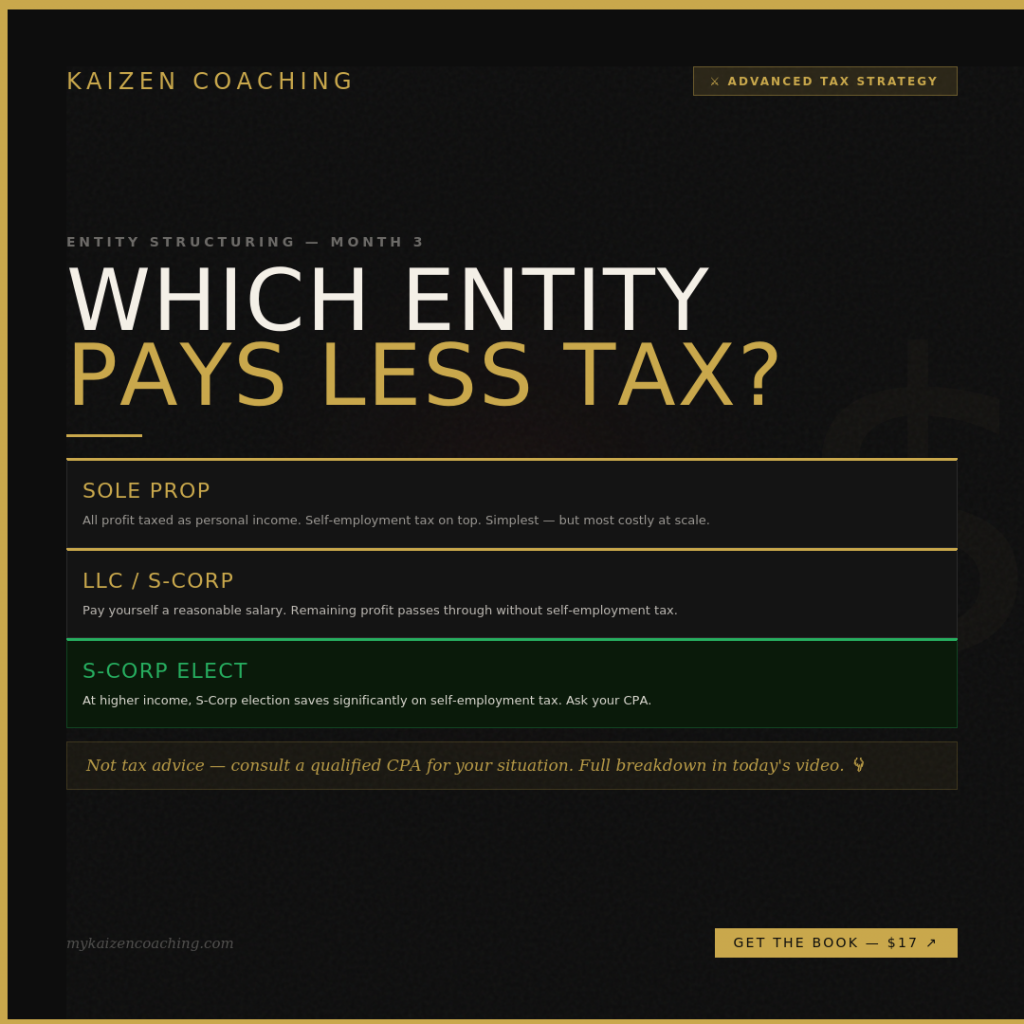

The Entity Structure Conversation You Probably Haven’t Had

Most self-employed people operate as sole proprietors by default. It’s automatic — no paperwork, no setup. Every dollar of business profit is personal income, and you pay self-employment tax of 15.3% on top of your regular income tax. That 15.3% covers Social Security and Medicare contributions.

Many people take the next step and form an LLC. This is a good move for liability protection — but here’s what most people don’t realize: by default, a single-member LLC is taxed exactly the same as a sole proprietorship. Forming the LLC alone doesn’t change your tax situation.

The tax change happens when an LLC elects S-Corporation status. Under an S-Corp election, you pay yourself a reasonable salary (which is subject to payroll taxes like any employee). The remaining profit passes through to you as a distribution — and distributions are not subject to self-employment tax.

At the right income level, that difference is meaningful. The general guideline: the S-Corp election tends to produce savings when net self-employment income exceeds approximately $40,000–$50,000 per year. Below that threshold, accounting costs may offset the tax benefit.

The question to ask your CPA: Given my current net self-employment income, would an S-Corp election produce tax savings that outweigh the additional accounting and payroll costs?

Self-Employed Retirement Accounts: The W-2 Blind Spot

Most W-2 employees are familiar with two retirement vehicles: the employer 401(k) with a contribution limit around $23,000/year, and the Roth IRA with a limit around $7,000/year.

Self-employed people have access to accounts that most employees don’t.

Solo 401(k): As a self-employed person, you are both the employer and the employee. That means you can contribute on both sides. Employee contributions follow the standard $23,000 limit. Employer contributions can be up to 25% of compensation. Combined, the total annual contribution limit reaches approximately $69,000 (verify current IRS limits — they adjust annually). Every dollar contributed is a deduction against your taxable income.

SEP IRA (Simplified Employee Pension): Contribute up to 25% of net self-employment income, up to the annual maximum. Simpler to set up than a Solo 401(k) and a good starting point for those new to self-employed retirement planning.

SIMPLE IRA: Lower contribution limits but simpler compliance requirements. Better suited for small businesses with employees.

The critical point: these contributions reduce your taxable income dollar-for-dollar. A $30,000 Solo 401(k) contribution doesn’t just save for retirement — it reduces the income you pay tax on this year.

The question to ask your CPA: Can you help me set up a Solo 401(k) or SEP IRA, and what is the maximum I can contribute this year based on my net self-employment income?

The Home Office Deduction — Two Methods, One Right Answer for You

The home office deduction is one of the most commonly missed — and most commonly misunderstood — deductions available to anyone who operates a business from home.

There are two calculation methods:

Simplified Method: $5 per square foot of dedicated office space, up to 300 square feet. Maximum deduction: $1,500 per year. Fast, minimal documentation.

Actual Expense Method: Calculate the percentage of your home dedicated to business use (office square footage ÷ total home square footage). Apply that percentage to your actual home costs: rent or mortgage interest, utilities, insurance, and repairs. For most homeowners, this method produces a deduction two to three times larger than the simplified method.

The non-negotiable requirement: the space must be used regularly and exclusively for business. A dedicated office qualifies. A kitchen table where you occasionally work does not. A guest room that doubles as storage does not. The IRS applies this standard strictly.

If you’re currently using the simplified method, ask your CPA to run the actual expense calculation for your home costs and office percentage. The difference may surprise you.

The question to ask your CPA: Based on my home costs and office square footage percentage, would the actual expense method produce a larger deduction than the simplified method for my situation?

Bringing It Together: The CPA Meeting You Should Schedule This Week

Most people go to their CPA at tax time with a shoebox of receipts and a hope that nothing is wrong. The CPA’s job in that scenario is compliance — filing an accurate return.

The CPA’s job in a strategic relationship is different: proactively identifying the legal structures and accounts that produce the best outcome for your specific situation. To access that, you have to ask the right questions.

Here’s a short list to bring to your next meeting:

- Given my current income, would an entity structure change produce tax savings?

- What self-employed retirement accounts should I be contributing to, and what’s my maximum this year?

- Am I using the right home office deduction method?

- Are there any deductions specific to my business type or industry that I might be missing?

That last question is an open-ended prompt that often surfaces things CPAs know about but don’t proactively mention unless asked.

The Bottom Line

The basics — tracking expenses, logging mileage, deducting your phone — are a good start. But they’re the surface of what’s available to self-employed people under the tax code.

Entity structure, retirement account contributions, and the right home office method are where the meaningful differences live. None of this is complicated once you know what to ask. And knowing what to ask starts here.

Not tax advice. This is educational overview — consult a qualified CPA for guidance specific to your situation. Contribution limits referenced are approximate and change annually — verify current IRS figures with your advisor.

Jeremy Jenkins is a lifestyle and wealth coach and the founder of Kaizen Coaching. The Kaizen Wealth Operating System — a 15-chapter field manual for fighting back against the 5 enemies of wealth — is available at mykaizencoaching.com for $17.