We treat a steady job as the definition of financial safety. Get the stable position, keep it, and you’re secure. But there’s a crack running straight through that idea, and once you see it you can’t unsee it: a single income is a single point of failure.

If everything you have flows from one source, then the health of your entire financial life depends on one thing never going wrong. One layoff. One industry downturn. One illness. The paycheck that felt like safety turns out to be the most concentrated risk most people will ever take — and almost no one names it. That’s the fourth enemy of wealth.

Stability Is Not the Same as Security

A stable job can still be a fragile foundation, because stability describes how things feel right now, while security describes what happens when something breaks. You would never put 100% of your savings into a single stock and call it safe. Yet a single income puts 100% of your financial security into one source. Diversifying your income, it turns out, matters just as much as diversifying your investments.

Financially secure households tend to understand this instinctively. They rarely depend on one source. There’s usually a primary income, but also some combination of a side business, dividends from invested assets, a rental, a royalty, or interest. Several streams, arranged so that no single failure can sink the whole ship.

The Two Ways to Make Money

Almost nobody is taught the most important distinction in personal finance: there are only two ways to make money.

The first is to trade your time for it. A job, an hourly role, most freelancing. You show up and you’re paid; you stop and the money stops. This is active income, and it has a hard ceiling — there are only twenty-four hours in a day, and you cannot sell hours you do not have.

The second is to build or own something that pays you whether you show up or not. A business that doesn’t need you in every seat. Dividends from assets you own. A rental. A royalty. A digital product. This income isn’t capped by your hours, and it’s where lasting wealth is actually built.

Most people spend their entire working lives mastering the first kind and never start the second — not because they’re incapable, but because no one ever told them the second kind was the goal. The move that changes everything is to use active income as fuel: trade time for money, use that money to acquire assets, and let the assets begin to pay you.

The Income Ladder

Getting off a single income isn’t about motivation; it’s about following a path. Picture it as a ladder with four rungs.

Rung one is to max out your main stream — raises, negotiation, and skills that increase your value. This is your launch pad and your funding source. Rung two is to add an active side stream you run yourself: a side business, a service, a skill you sell. It still trades time for money, but it’s yours, and it becomes the seed capital for everything above it. Rung three is the leap from earning to owning: convert the income from rungs one and two into assets that pay you without your hours. Rung four is to reinvest, feeding the income from your assets back into more assets, until the process compounds — money making money making money.

Most people spend their whole lives on rung one. There is nothing wrong with rung one. It simply was never meant to be the entire ladder.

A fair word on vehicles: there are countless ways to climb rungs two and three — side businesses, dividend investing, real estate, digital products, and partnership models among them. Each carries its own mix of effort and risk, and none is a shortcut. The right one depends on your life, your skills, and your tolerance for risk, which is a decision only you can make.

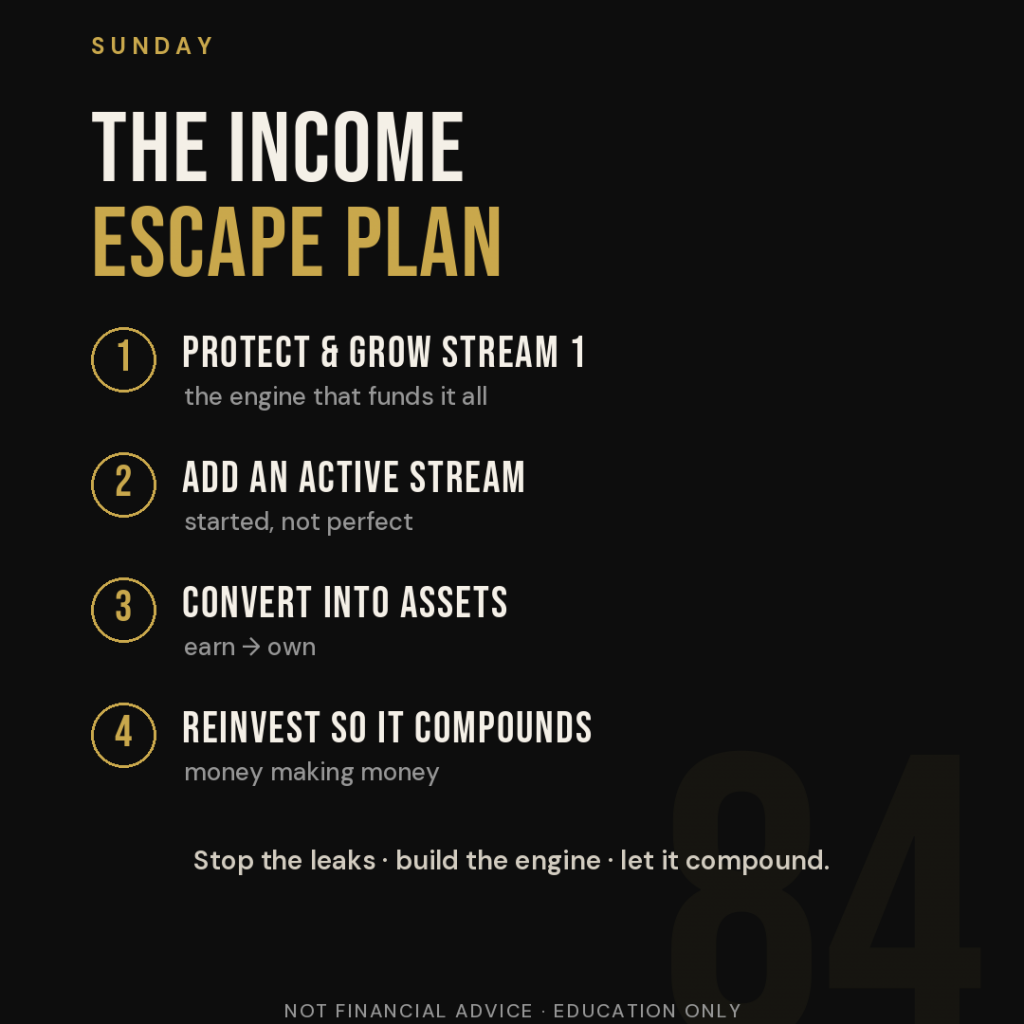

The Income Escape Plan

Pull it together and it becomes one repeatable system. Step one: protect and grow stream one, because it funds everything else. Step two: add an active stream — started, not perfect. Step three: convert that income into assets that pay you without your hours. Step four: reinvest so it compounds, until the snowball finally rolls in your favor instead of against you.

That last image connects this enemy to all the others. The first three enemies — taxes, inflation, and debt interest — are about stopping leaks in what you already have. Building income is about constructing the engine. And compounding is what carries that engine through the ups and downs of market volatility over time. Stop the leaks, build the engine, let it compound.

The Kaizen Bottom Line

You don’t escape a single income in one dramatic leap, and you almost certainly don’t do it by simply working more hours — that’s just renting out more of the one thing you can’t make more of. You do it the way you beat every enemy of wealth: one small, deliberate step at a time. Count your current streams honestly. Pick one direction for a second. Take the first small step this week. Then take another. Built patiently, a second stream — and eventually a third — turns a fragile foundation into a resilient one.

Not financial advice — this is educational overview. Building additional income takes real work and carries real risk, and any specific vehicle should be evaluated carefully. Consult a qualified professional for guidance specific to your situation.

Jeremy Jenkins is a lifestyle and wealth coach and the founder of Kaizen Coaching. The Kaizen Wealth Operating System — a 15-chapter field manual for fighting back against the 5 enemies of wealth — is available at mykaizencoaching.com for $17.