Of the five enemies of wealth, the last one is the strangest. Taxes take your money through a bill. Inflation takes it through prices. Debt interest takes it through a payment. But market volatility — the fifth and final enemy — rarely takes anything directly. It does its damage by convincing you to hand your money over yourself.

The pattern repeats in every cycle. Markets swing, because that is what markets do. And people buy near tops, because everything feels wonderful, then sell near bottoms, because everything feels terrifying. The swing didn’t cost them. The reaction did. The market didn’t take their money; panic did.

Volatility Is Not Risk

The most useful distinction in all of investing is also the least taught: volatility and risk are not the same thing.

Volatility is movement — the market going up, down, and sideways, sometimes violently. It isn’t a malfunction. Swings are the system working, not the system breaking. Risk is something else entirely: the chance that you permanently lose money.

Here’s the uncomfortable part. For long-term investors, the biggest source of permanent loss historically hasn’t been the swings themselves — it’s been the reaction to them. A dip only becomes a loss when you sell it. There’s even a name for the damage: the behavior gap, the well-documented difference between what investments return and what investors in those investments actually earn, caused by buying high in euphoria and selling low in fear. Same asset, worse outcome, purely because of behavior.

Zoom out and the picture changes completely. The same market that looks like chaos day to day has historically looked like a trend with wiggles in it over years and decades. Every major downturn so far has shared one shape: it looked like the end while it was happening, and like a blip in hindsight. History isn’t a promise about the future — but it’s a far better teacher than a panicked headline. Volatility, as the saying goes, transfers money from the impatient to the patient.

The Volatility Defense Kit

You cannot control the market. You can control four things — and none of them require predicting anything.

The first is a long time horizon. Storms shrink as timelines stretch; a drop that’s terrifying over a month has historically been a wiggle over a decade. Time doesn’t remove volatility — it removes volatility’s power over you.

The second is real diversification. Not five versions of the same bet, but genuinely different things, so that no single basket hitting the floor can break you. If that sounds familiar, it should: it’s the same principle as building multiple income streams. Enemy #4 and Enemy #5 are cousins.

The third is automatic investing — putting the same amount in on a schedule regardless of what the market is doing, a practice often called dollar-cost averaging. Its power isn’t mathematical magic; it’s emotional. It removes the decision, and with it, the thing panic needs to operate.

The fourth is a cash buffer. An emergency fund isn’t just safety — it’s strategy. Most panic-selling isn’t really fear; it’s people who needed the money. When life goes sideways and the buffer pays for it, you are never forced to sell investments in a dip. The buffer breaks the trap before it springs.

Notice what isn’t in the kit: predicting, timing, watching financial news, or checking a portfolio daily. All four tools work precisely because they don’t require knowing the future.

The most powerful move of all may be the simplest: a dip plan, written in advance. One sentence — “when the market drops, I will __” — completed while nothing is on fire. A plan written in calm weather doesn’t flinch in a storm. A plan improvised mid-storm usually is the flinch.

The Overlooked Hedge: Income

Ask what the best hedge against a rough market is and you’ll hear the usual answers — gold, bonds, cash. The answer almost nobody gives: income.

Consider who actually suffers in a downturn. Rarely the person with steady cash flow — their bills are paid and their plan keeps running. The person who suffers is the one forced to sell because the paycheck stopped and the portfolio was the only money left. When income keeps flowing, a dip is a detail. When it doesn’t, a dip is a disaster. Same market, different income situation — which is why building multiple streams isn’t just growth, it’s defense.

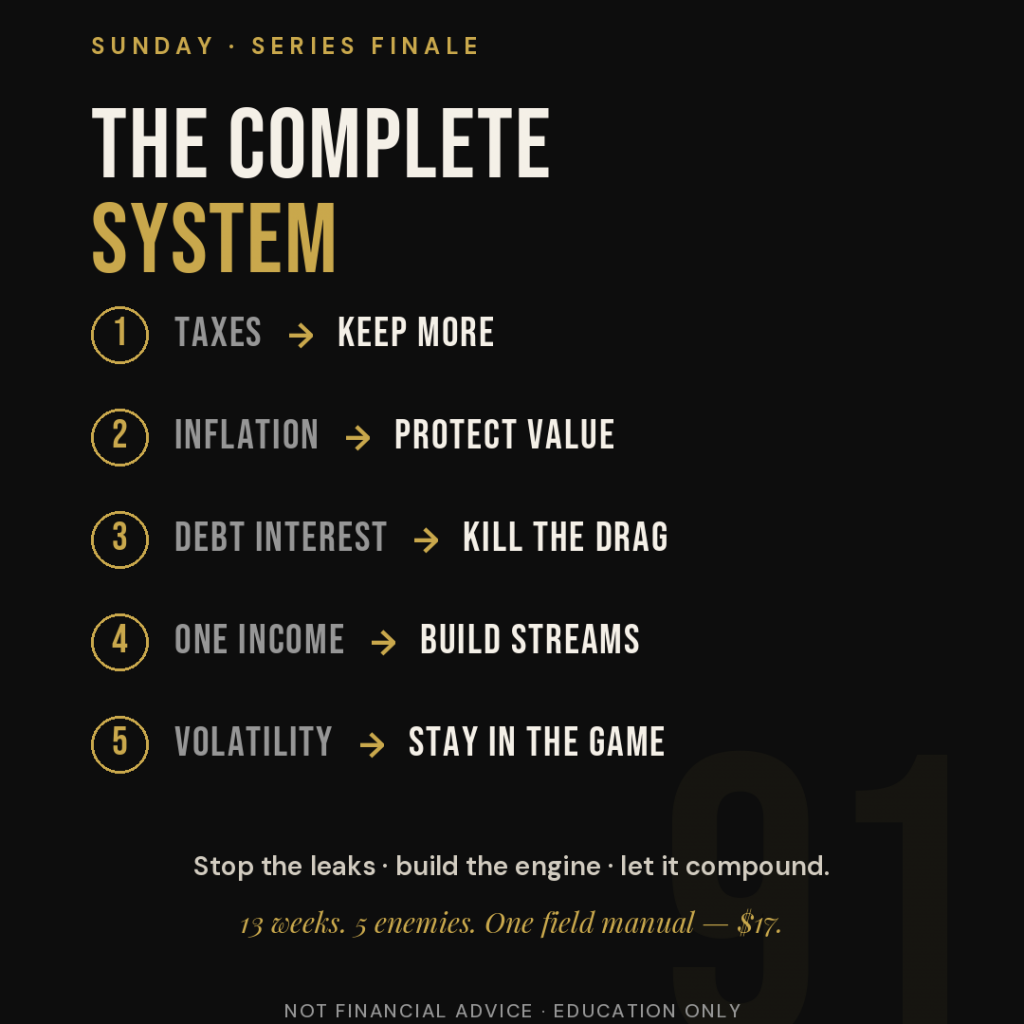

The Complete System

With the fifth enemy named, the whole map is on the table. Taxes are beaten by keeping more — capturing every legal deduction instead of tipping the government out of inattention. Inflation is beaten by protecting value rather than letting savings quietly melt. Debt interest is beaten by killing the drag — mapping the debt and pointing compounding back in your direction. A single income is beaten by building streams — earn, add, convert to assets, reinvest. And volatility is beaten by staying in the game with a plan written before the storm.

Stop the leaks. Build the engine. Let it compound. Every one of the thirteen weeks behind this post fits inside those three moves — and so does essentially every good piece of personal-finance advice you’ll ever hear.

The Kaizen Bottom Line

The final enemy isn’t out there in the market; it’s in the mirror, on a bad day, with a scary headline open. Which is oddly good news — because your behavior, unlike the market, is fully within your control. You don’t have to outsmart anything. You have to outlast your own fear, with a long timeline, real diversification, automatic habits, a cash buffer, and a one-sentence plan written while things are calm. One small, deliberate step at a time — the same way every enemy on this list gets beaten.

Not financial advice — this is educational overview based on how markets have historically behaved, which is not a guarantee of future results. Investing involves real risk, including loss of principal. Consult a qualified professional for guidance specific to your situation.

Jeremy Jenkins is a lifestyle and wealth coach and the founder of Kaizen Coaching. The Kaizen Wealth Operating System — a 15-chapter field manual for fighting back against all 5 enemies of wealth — is available at mykaizencoaching.com for $17.