Everyone has heard that compound interest is the eighth wonder of the world. It’s usually said with a smile, in the context of saving and investing — money that earns money, growing on itself, year after year.

Almost no one mentions the other half of that sentence. Because the exact same force that builds wealth when it’s pointed in your favor quietly destroys it when it’s pointed the other way. That’s debt interest. And it’s the third of the five enemies of wealth.

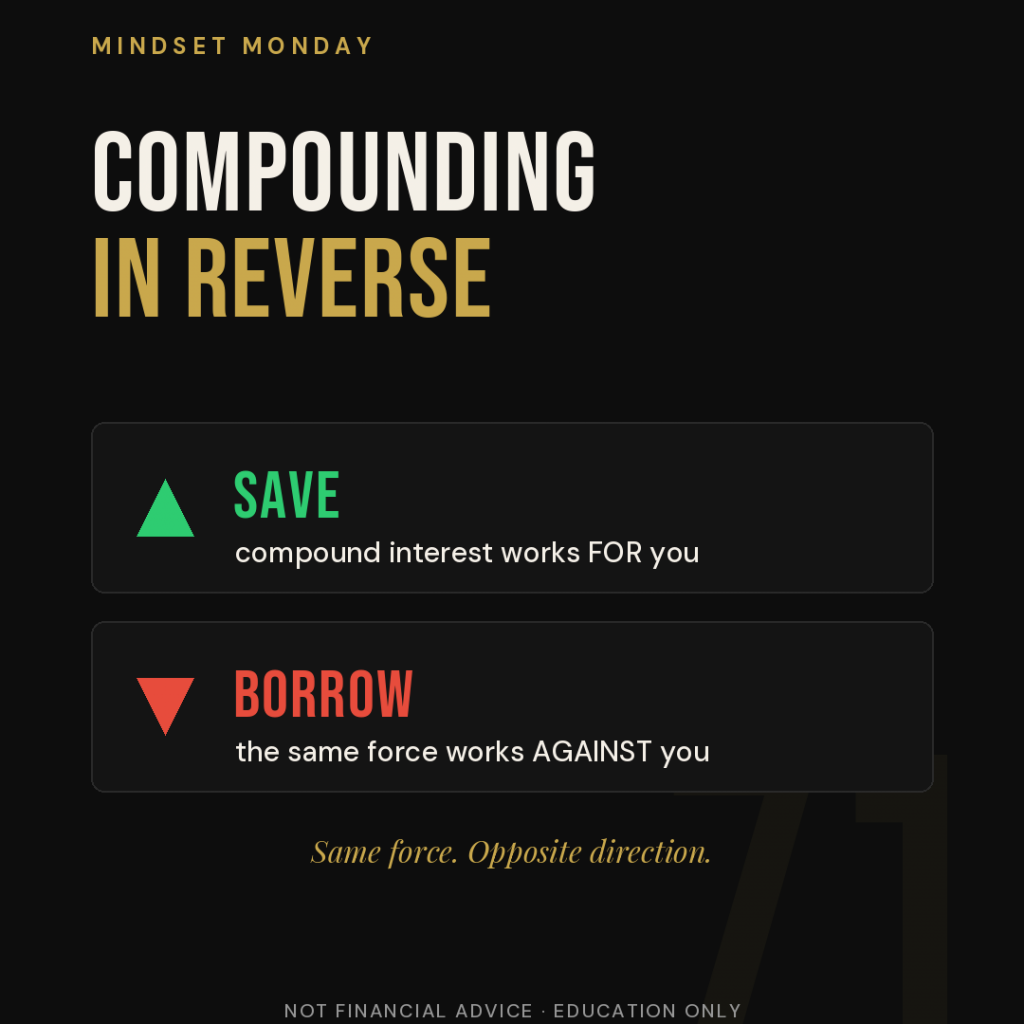

Compounding in Reverse

When you save and invest, compounding works for you — a snowball rolling downhill, getting bigger on its own. When you borrow, the identical force runs in reverse. Interest compounds against you, and you become the snowball someone else is rolling downhill.

Most people have this force pointed the wrong way without ever consciously deciding to. A mortgage. A car loan. A couple of credit cards. Student loans. Each one is compound interest aimed squarely at their future. The monthly payment is what they feel. The interest is what’s actually happening — and over the life of a loan, it can quietly cost more than the thing that was bought.

The reframe matters because it changes the goal. The enemy isn’t the borrowing itself. It’s the direction of the compounding — and direction can be reversed.

Amortization: Paying Rent on the Money

Here’s the number the lender never puts in front of you: amortization. On most loans your payment stays flat, but what that payment does changes dramatically over time. In the early years, the large majority of every payment goes to interest, and only a sliver reduces what you owe.

So in the first years of a typical 30-year mortgage, you can send the bank hundreds of dollars a month and watch your balance barely move. You’re not really paying down the house yet — you’re paying rent on the money. Over the full life of a long mortgage, the interest paid on top of the price can climb toward the price of the home itself, depending on the rate.

Understanding this reveals the leverage point: extra payments made early are extraordinarily powerful, because they attack principal before years of interest can stack on top of it. Even small amounts aimed at principal can erase months or years of payments at the back end.

The Minimum-Payment Trap

The single most expensive habit in personal finance is paying only the minimum — and it isn’t an accident, it’s a design. A minimum payment is calculated to cover the interest plus a tiny sliver of principal, just enough that the balance crawls down while interest keeps compounding on the rest.

On a high-rate card, paying only the minimum can stretch a balance into a decade or more of payments, and the total interest can end up rivaling or even exceeding the original amount charged. You didn’t buy the item once; you bought it, plus a second one for the bank.

Avalanche, Snowball, and the Roll

There are two proven ways to attack debt. The avalanche method lists debts by interest rate, highest first, and attacks the most expensive interest while paying minimums on the rest — mathematically the cheapest path. The snowball method lists debts by balance, smallest first, for quick wins that build momentum — slightly more expensive in interest, but far more likely to be finished, because motivation matters as much as math. The best method is the one you will actually stick with.

What makes either one accelerate is the freed-cash-flow roll: as each debt dies, you don’t absorb its payment back into spending — you redirect the entire freed-up payment to the next debt. Each payoff makes the next one faster, until the snowball is finally rolling in your favor.

For those who want to go further, an advanced layer exists: interest cancellation. By routing income through a line of credit and reducing the average daily balance that interest is charged on, it’s possible to pay down principal faster without earning an extra dollar. Tools like United Financial Freedom’s software are built around mapping this kind of efficient payoff path for a specific set of debts. It’s worth understanding and evaluating carefully — not a guarantee, and never a substitute for the fundamentals.

The Lever With No Ceiling

Cutting your budget to throw more at debt works, but it has a floor — you can only cut so much. The income side has no ceiling. Every extra dollar earned and aimed at principal does double duty: it removes the balance and all the future interest that balance would have generated.

This is where Enemy #3 quietly connects to Enemy #4. The fastest path out of debt interest often runs through building additional income — and the strongest plans don’t treat “pay off debt” and “build income” as separate seasons. They run them together.

The 5-Step System

Put it all together and it becomes one repeatable system. First, see it all — list every balance, rate, and minimum in one place. Second, free up cash flow — find the gap between income and spending. Third, attack in order — avalanche or snowball, all freed cash at one debt. Fourth, roll the payments — each dead debt funds the next. Fifth, raise the ceiling — add income, aim it at principal, and keep it building after the debt is gone so freed cash flow becomes wealth instead of new spending.

The Kaizen Bottom Line

You don’t beat debt interest in one dramatic move. You beat it the way you beat every enemy of wealth — one small, deliberate step at a time. Write down what you owe. Decide which debt is first in line. Pay one dollar more than the minimum this month. Small steps, stacked consistently, until the most powerful force in your finances finally runs in your direction.

Not financial advice — this is educational overview. Figures are illustrative, and tools mentioned are for awareness, not endorsement. Consult a qualified professional for guidance specific to your situation.

Jeremy Jenkins is a lifestyle and wealth coach and the founder of Kaizen Coaching. The Kaizen Wealth Operating System — a 15-chapter field manual for fighting back against the 5 enemies of wealth — is available at mykaizencoaching.com for $17.